Updated Thoughts on Some of My Biggest Positions In The Cheap Japanese Basket and Some New Positions

Thoughts on Dynam Japan, Keihin, Somar, Takigami Steel, Fujishoji, Integral, and Hyoki Kaiun Kaisha

Let’s start with a new name in the Japanese basket.

Dynam Japan (SEHK 6889)

Market cap: HK$ 2.31 billion ($296 million USD)

Dynam Japan is the largest operator of Pachinko halls in Japan. The company has been profitable for the past15 years, though profits have been in decline. Their halls are mostly located in suburban areas with less competition, but they do have some in big cities. The company is listed in Hong Kong as the pachinko business is a legal gray area in Japan.

P/B: 0.4

P/E (forecast): 10

Dividend Yield: 7.6%

Dynam bought back ~9% of shares since 2020 and pays out a decent dividend. The company was sitting on a massive net cash position until 2019 when they began purchasing airplanes to get into the airplane leasing business. Yes, you read that correctly. A pachinko hall operator decided to get into the airplane leasing business.

Net cash went from ¥44 billion to net debt of ¥154 billion (interest bearing debt stands at ~¥92.4 billion today. The ¥154 figure includes lease and other liabilities). The company began purchasing airplanes around 2019, right before covid with their first 4 airplanes being leased as follows:

While this pivot is extremely odd, it may prove timely as prices of airplanes and their lease rates have increased since Covid due to production issues at Boeing and Airbus. Dynam owns 10 new airplanes (average age 2.4 years). The debt associated with airplane purchases are non-recourse to the rest of the company too.

Dynam also manages 7 aircraft for other parties. While I find this pivot to be extremely strange, it’s a better use of their cash than just sitting on it, which is what most Japanese corporations seem to prefer.

The timing of this pivot to airplane leasing could be a winner for Dynam as not only have airplane prices increased, but they’re priced in USD which has appreciated vs JPY. I could be wrong here, but Yen weakness also understates book value as the airplane assets are valued in USD, but Dynam records them on the balance sheet in JPY at the time of purchase. The first 4 planes were bought when USD/JPY was 105-110 vs 155 today.

Some portion of the company’s interest bearing debt is in JPY according to the annual meeting document where the company says they took out ¥10 billion in JPY debt last year to invest in aircraft leasing and other growth opportunities. The remainder of the borrowings are likely in USD and EUR as these are the primary currencies used in the aircraft leasing business. A breakdown of liabilities by currency was not spelled out in their disclosures, but interest bearing debt / interest expense comes to ~3.3% annualized.

While the core Pachinko hall business is competitive and in decline, Dynam’s size gives them some competitive advantages. Besides just getting better pricing given their size, the company also develops their own in-house Pachinko/Pachislot machines. They also partner with manufacturers for exclusive machines, something small to mid operators cannot do.

Dynam Japan pays for sponsored research which explains their business in depth (in English). I recommend checking it out here. They also publish earnings presentations and annual reports in English. Despite the ~$300m usd market cap, the stock is extremely illiquid.

Activism isn’t possible here as two board members Yoji Sato and his wife Kohei Sato collectively control 59% of outstanding shares. While the stock has done poorly in the past, the company is dirt cheap today and the market is sleeping on the asset value of the airplanes (which are held at cost in JPY and depreciated).

This is a basket sized position for me, so I haven’t dug too deep. I just know it’s cheap. The buybacks and dividends also provide some comfort that management at least cares a bit about shareholders. A sub-scale airplane leasing business attached to a pachinko hall operator is certainly bizarre, but the stock is cheap.

I own a basket sized position in Dynam. I’ve also been to one of their parlors in Tokyo (and lost ¥10,000). If anyone does a NAV calculation for Dynam’s aviation assets, please leave it in the comments section!

Keihin Corp (TYO 9312)

Market cap: ¥13.9 billion

I remain optimistic about Keihin and Nissin Corp, my two favorite Japanese logistics companies. Nissin Corp has performed well, executing significant share buybacks and raising their dividend. Meanwhile, Keihin remains deeply undervalued. Management has signaled they will address the TSE’s request regarding ‘cost of capital and stock prices’ by May 2025. This can be seen in the following message they sent me:

Here’s a quick recap to contextualize Keihin's undervaluation:

20 years ago Keihin was trading at 1.2x book value and 21x P/E, with ¥25.3 billion in net debt. Earnings per share (EPS) stood at ¥96, and the stock price was ¥2,000, giving it a market capitalization of ¥13.5 billion.

Today, the stock price is nearly unchanged at ¥2,130, despite the company having paid off all of its net debt (with no dilution) and tripling its EPS.

P/E today is 6.5 (EPS LTM ¥327)

P/B today is 0.4

Dividend yield is 3%

Keihin has been improving its balance sheet while growing profits for 20 years. It was expensive in 2004, today its dirt cheap and its warehouse assets are worth much more than carrying value.

These 3 images below illustrate just how much Keihin’s fundamentals have improved with virtually no change in share price.

Hopefully management unveils an improved capital allocation plan in May in response to the TSE.

Keihin and Nissin Corp are both top 3 positions in my cheap Japanese basket.

Somar Corp (TYO 8152)

Market cap: ¥11.4 billion

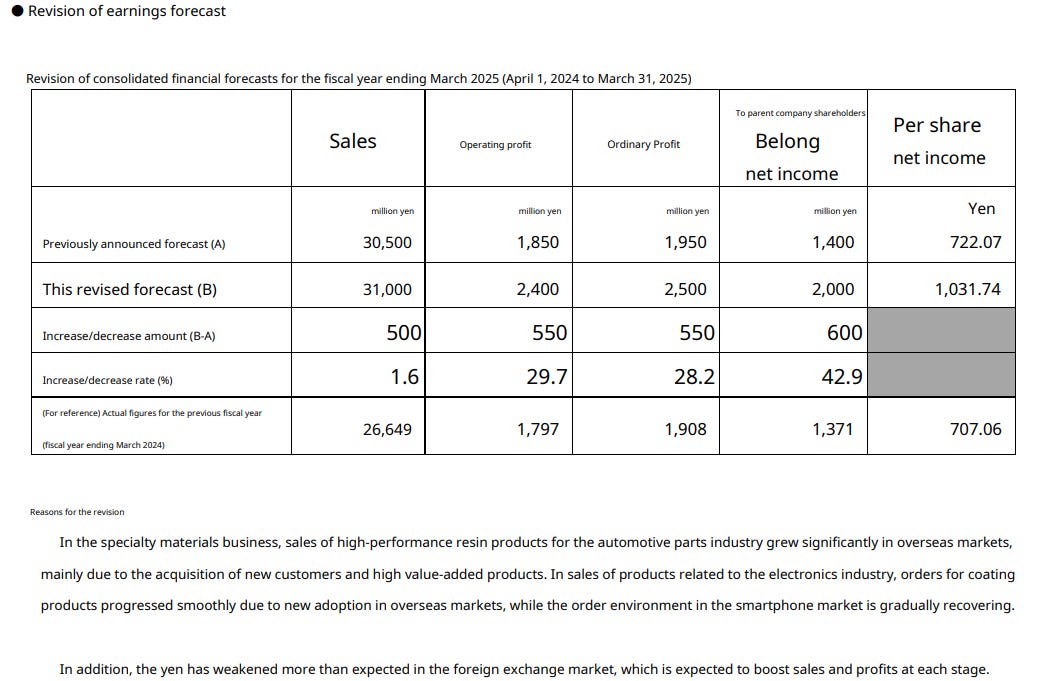

This is a name that’s been in my basket for some time now, but I’ve never written about it. It’s a dirt cheap net-net that’s trading at 0.6x price to book despite rapid growth. My original purchase is up about 100%, but I recently added to my position when the stock dipped 5% after their last earnings report. While it’s always hard to add to a position that’s up 100%, seeing the stock dip 5% after Somar revised net income per share guidance from ¥722 to ¥1031 per share (PE: 5.7) was just too enticing. Remember, this is a net-net!

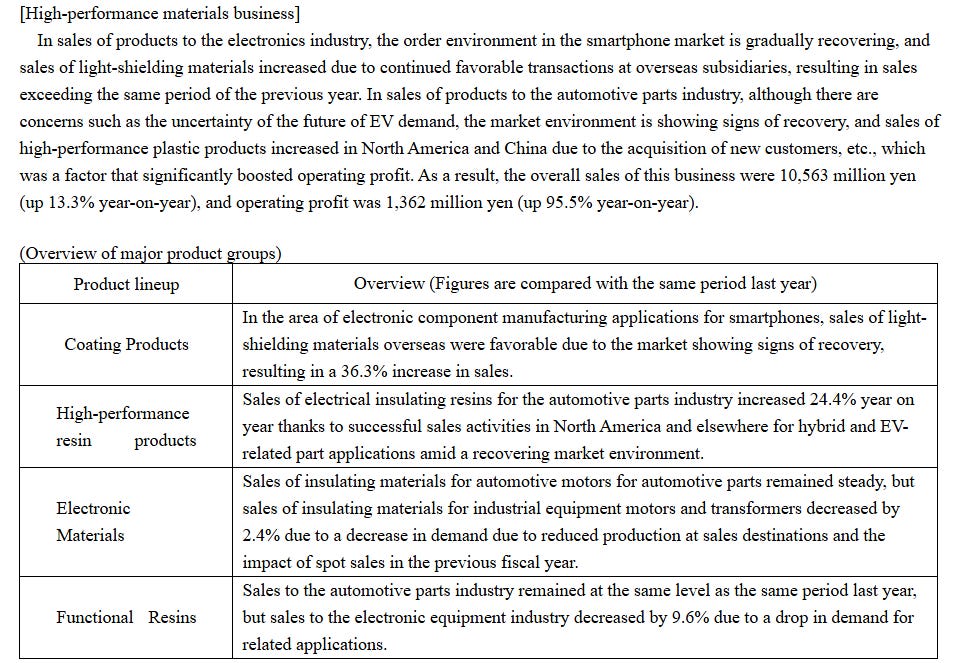

The company also feels optimistic enough about their future prospects to open a manufacturing facility in the United States (in West Virginia). The company’s major product segments can be seen below:

Somar is a top 3 position in my cheap Japanese basket.

Takigami Steel Construction (TYO 5918)

Market cap: ¥18.5 billion

This idea is still pretty new and it has run up pretty quickly since my writeup on Dec 6 (from ¥6,050 to ¥8,260). While the runup was likely due to my writeup, there’s still significant upside with NCAV+Investments being worth about ¥18,000 /share. I still have no idea who Evergreen Investments is (the #2 shareholder with 11.42% of outstanding shares). This is dirt cheap with easy to value assets.

I owned 1,200 shares when I did my writeup and I still have 1,200 shares today. This is an extremely illiquid stock with bid/ask spreads routinely 5-10%.

Fujishoji (TYO 6257)

Market cap: ¥28.27 billion

Fujishoji is a consistently profitable net-net manufacturer of Pachinko and Pachislot machines (though they did report a loss during covid). While the entire Pachinko/Pachislot industry has likely been over earning a bit post-covid, the company expects to earn ¥177 per share for the fiscal year ended March 2025 for a P/E of 7.64. The dividend yield is also a respectable 4%. A net-net with 7.64 P/E alone is enticing, but what makes Fujishoji even more interesting is its a net-net excluding its investment securities which are worth ~¥10 billion. Investment assets are made up of the following:

Suncorp stake (6736) = ¥8.6 billion (940,000 shares)

Gamecard stake (6249) = ¥1.5 billion (611,900 shares)

Longterm prepaid expenses = ¥2.4 billion

Let’s add NCAV to this total to get a conservative valuation for the company (while valuing the actual business that set to earn ¥3.7 billion this year at zero)

NCAV = ¥27.5 billion

Total = ¥40 billion

Market cap= ¥28.27 billion

Fujishoji owns ~¥8.6 billion of Suncorp stock. Suncorp’s value is tied to the fortune’s of Nasdaq listed Cellebrite (CLBT) as Suncorp owns 46% of CLBT, which is worth ¥327 billion (vs Suncorp’s market cap of just ¥204 billion). Suncorp trades at a significant discount to its ownership in CLBT, but given the activists involved in Suncorp (Oasis management), that value may eventually be realized, which gives a bit of upside to Fujishoji’s ownership in Suncorp. Fujishoji’s Suncorp investment has ballooned in value from just ¥3.1 billion in March to ¥8.6 billion today while the stock has remained flat.

Sun Corp is also a decent bet on its own given the activist involved.

I own shares in both Fujishoji and Gamecard.

Integral Corp (TYO 5842)

Market cap: ¥134.4 billion

Integral Corp is a Japanese private equity firm that IPO’d in late 2023. I only discovered the company after they bought a 49% stake in Mutoh Holdings (TYO 7999) back in November 2024. They purchased the stake from the company’s founding family for around market price at the time, which is stupid cheap given that Mutoh is trading at net net valuations and a price to book of 0.5x. I have no idea why the founding family would sell their stake so cheaply. They basically gave the company away for free (net net valuation). I want to be on the other side of that transaction, so I bought a small stake in both Mutoh and Integral.

P/E (LTM): 10

P/B: 2.8

Integral provides English financials and presentations. It’s a thematic bet on private equity in Japan.

I own shares in both Mutoh Holdings and Integral Corp. Mutoh qualifies for inclusion in the ‘cheap Japanese basket’ while Integral is technically more of a traditional value stock with growth. It’s not deep value.

Hyoki Kaiun Kaisha (TYO 9362)

Market cap: ¥4.64 billion

This is a tiny logistics company that I was bullish on since I wrote about it in June 2024. It is up 63% from ¥2,400 to ¥3,910 since the writeup and there’s still significant upside. On October 10th Dojima Kisen, a private logistics/shipping company, made a tender offer to buy 17.8% of the company for ~¥3,250, which was a premium to the share price at the time. Few public shareholders tendered their shares and the stock has slowly climbed well above the tender price. The company took a neutral stance to the tender at first and later publicly opposed it and announced a capital alliance with Yamato Kogyo Co (TYO 5444), a much larger (~100x the size of Hyoki Kaiun Kaisha) public company in the Steel business as a way to counter Dojima Kisen. No word on what this capital alliance entails just yet.

The original tender led to Dojima Kisen acquiring just 1.24% of the company. Since the failed tender, they’ve been buying up shares on the open market at prices well above the tender offer. On January 7, 2025 Hyoki Kaiun Kaisha announced that Dojima Kisen had increased their ownership stake in the company from 7.52% to 10.16% between December 16, 2024 and December 23, 2024.

Dojima Kisen clearly sees value in Hyoki Kaiun Kaisha. In my own writeup I conservatively valued the company at ¥6,207/share, but the actual market price could be significantly higher. I’m not sure why Yamato Kogyo has shown interest in the capital alliance. Maybe they see value and are willing to work with management to keep Dojima Kisen out, which they might see as hostile. This is getting interesting! I’ve added to my position when the tender offer was first announced.

I own shares in Hyoki Kaiun Kaisha

This is not an exhaustive list of all my longs. I own way too many cheap Japanese companies to comment on all of them.

Disclosure: I own shares in the stocks mentioned. These securities could be sold at any point in time without prior notice. None of this is investment advice. Everything in this post is my own opinion and I could be wrong. Do your own due diligence.

Hey Altay,

Thanks as always for the write ups.

I built a net-net/ ideally NegEv basket in 2023 and am just revisiting it now (a little slow, I know. although I have sold some positions that moved a lot, over that time frame). Thought you might be interested in the few that haven't moved a whole lot yet.

I haven't run back over them properly yet but at the time I wanted them to most of the below boxes - ideally all:

- Net/Net, Ideally not made up of bloating AR or potentially difficult to shift/expiring inventory.

- Ideally negative EV or very close to.

- NCAV build over last decade (or at least not slipping).

- BV built over last years.

- Cash build, or at least not burning through their cash pile.

- 10+ years of profitability with slight leniency, particularly for one time events/write downs.

Some of these I've noticed you post about, some of them I haven't although you may well be aware of them. If not, they might be worth a quick look for you - some of these will have moved beyond my above criteria so i'll just post them from those that have moved least, to those that have moved most, of those i continue to hold for now for now.

7399 - Nansin.

8881 - Nisshin.

6964 - Sanko Corp.

4976 - Toyo Drilube.

7614 - OM2 Network.

7902 - Sonocom.

1879 - Shinnihon.

5958 - Sanyo Ind.

5078 - Cel Corp.

5658 - Nichia Steel.

7841 - Endo Manufacturing.

Hopefully there's one or two in there you haven't stumbled across and find interesting - although that's probably unlikely with how prolific you are with your JapCo hunting.

Anyway thanks again for the blog.

Thanks for sharing. Fantastic breakdown of opportunities. Completely agree on The Keihin Co - fascinating to see a company improve its fundamentals so dramatically over two decades yet still trade at these valuations. The upcoming TSE response adds an interesting catalyst to an already compelling story. Keep these gems coming!