Takasago Tekko (5458): A Profitable ¥3.3bn Nanocap near net-net @ 7.7x ntm P/E With ¥3.8bn of Appraised Rental Real Estate and a 36,009 sqm Tokyo Factory Site Carried at ¥2m (But worth ¥8bn+)

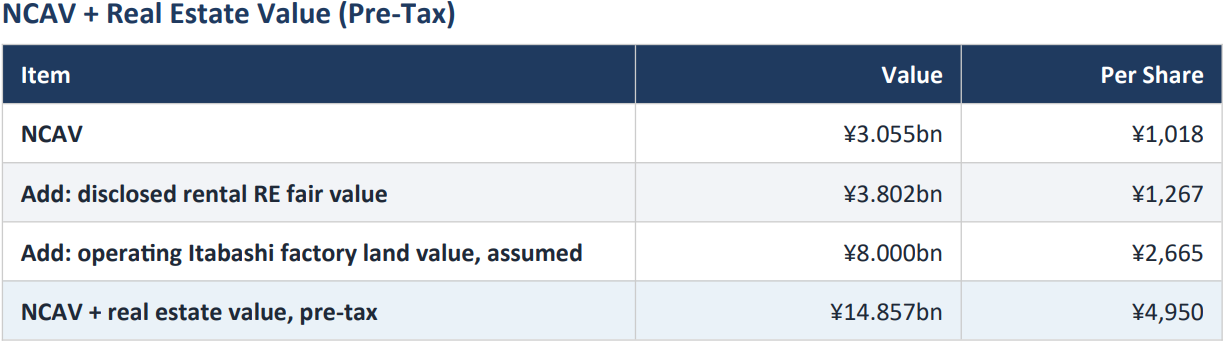

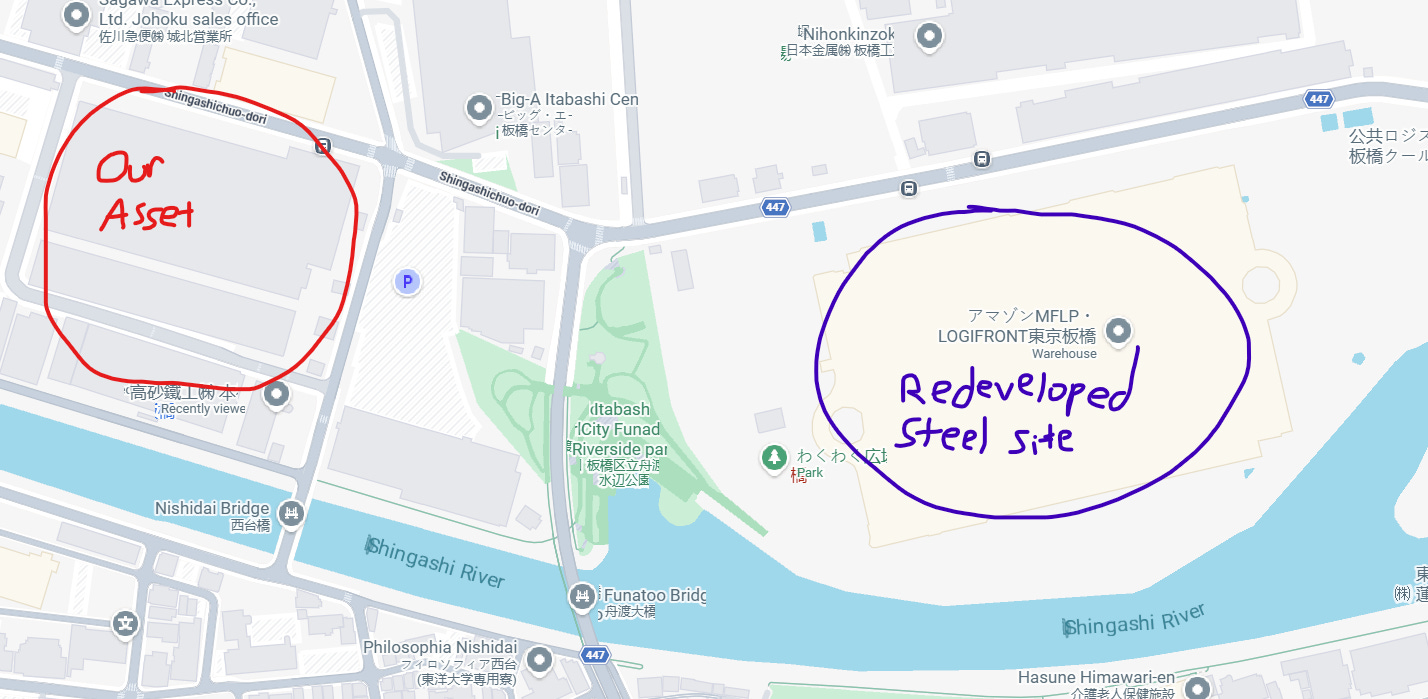

Factory site located in prime logistics hub where a previous steel site was redeveloped into major logistics project. Land could be worth ¥16bn+. We assume ¥8bn to be conservative.

Share Price: ¥1,120

NCAV: ¥1,081 /share

Market Cap: ¥3.37 billion

P/E (LTM): 9.5x

P/E (Management Forecast): 7.7x

Dividend: 4%

Thesis: Takasago Tekko (TYO 5458) is practically a net-net (and is one if you include investments) trading at ~9.5x LTM earnings (7.7x NTM) and has rental real estate worth ¥3.8 billion (more than the entire market cap) using the company’s own fair value disclosure. The story gets interesting when we consider the massive Itabashi Factory Land (36,009 sqm in Itabashi-ku Tokyo) which sits on the balance sheet at ¥2 million ($12,800 USD) but is conservatively worth ¥8 billion ($51 million). This is likely worth much more based on comps I found but we’ll use ¥8 billion to be safe. The facility was likely acquired around 1937, which is why it’s carried at near nothing.

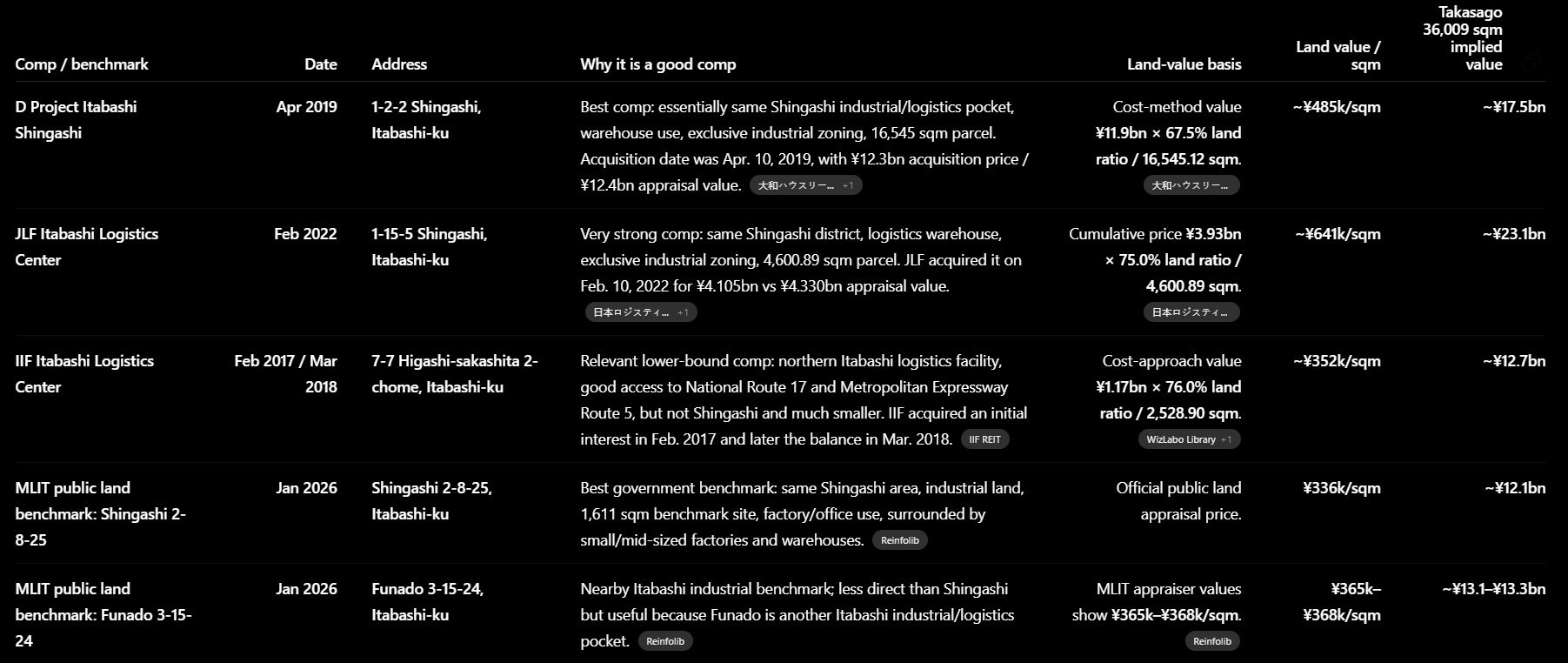

The estimate for Itabashi factory land is conservative. See Appendix for true market comps (It could be worth 50-150% more).

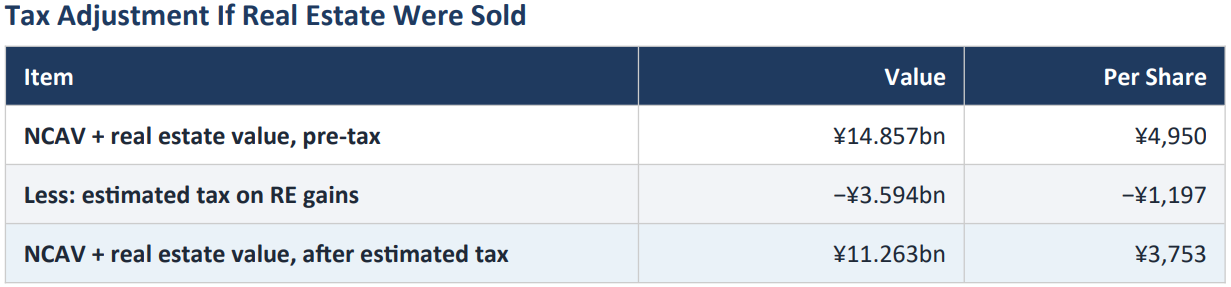

Pre-tax NCAV + real estate value: ¥4,950 /share

After-tax NCAV + real estate value: ¥3,750 /share

The Good:

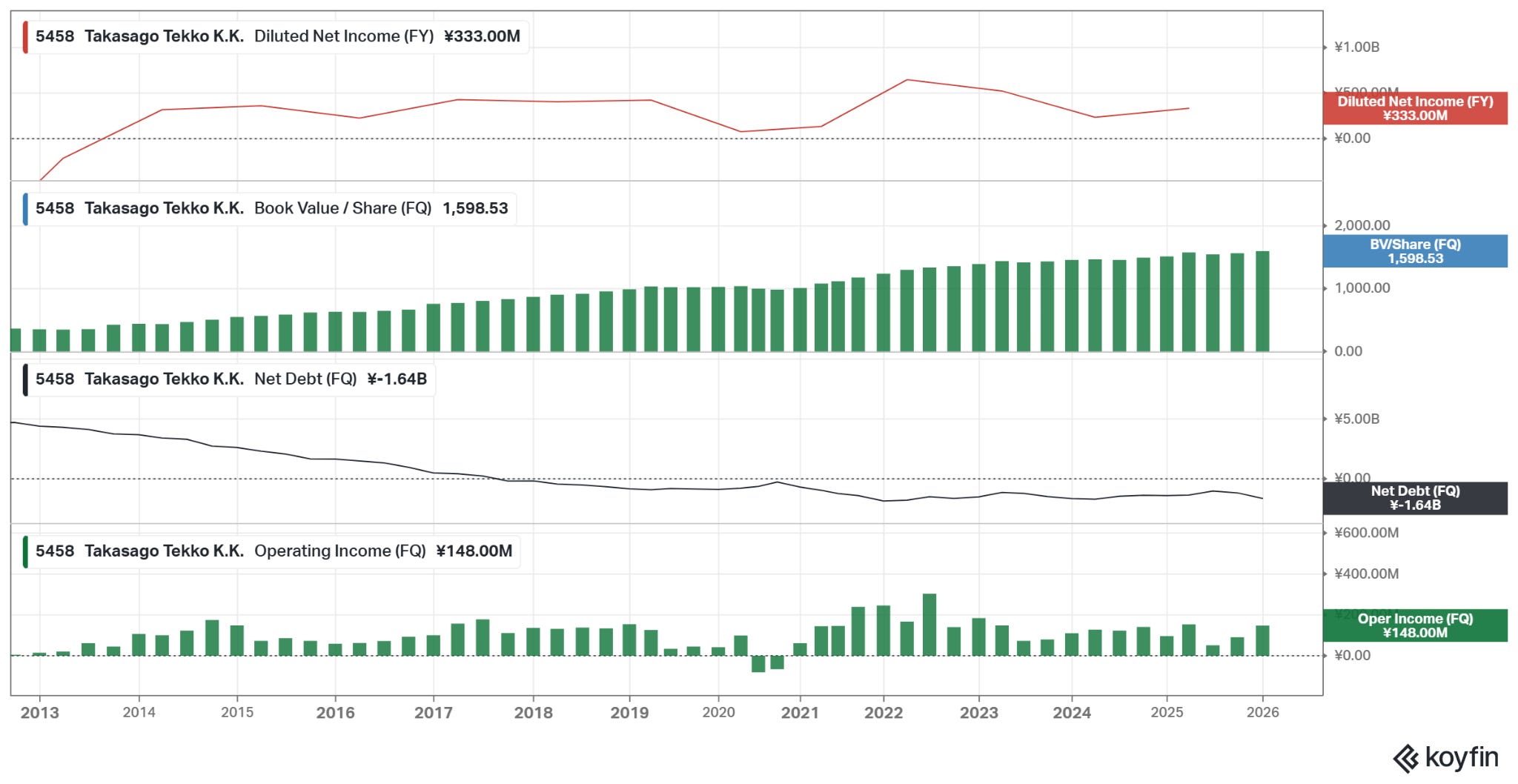

Consistently profitable since FY2014 (12 years of profitability) with strong FY27 profit forecast (7.7x p/e)

Net debt has decreased from ¥4.71 billion to net cash of ¥1.64 billion. FY26 report shows net cash of ¥2.3 billion.

Largely flat (slightly declining) share count

Few employees (~150), which makes transformation easier. Employees could be offered 2x annual pay to retire and it wouldn’t make a big dent in our massive asset base.

The 4% dividend makes holding this much easier.

Management is at least saying the right things. In its TSE capital efficiency disclosure, the company targets a 30%+ dividend payout ratio and 1.0x PBR, and explicitly acknowledges that PBR remains below 1.0x. The dividend has also doubled since FY2019, so there’s been some real improvement.

The huge Itabashi factory sits in a prime logistics hub in Tokyo. Another former steel site across the street from our factory was redeveloped into a modern logistics facility (see Appendix). Could be worth 2x my ¥8bn estimate.

Very under the radar stock. Only 5 posts so far in 2026 on Yahoo Finance JP board. No one is looking at this.

The Bad:

Steel adjacent business. Not commodity steel, but steel adjacent names have historically been value traps and rarely re-rate higher. This is a specialty processor / re-roller.

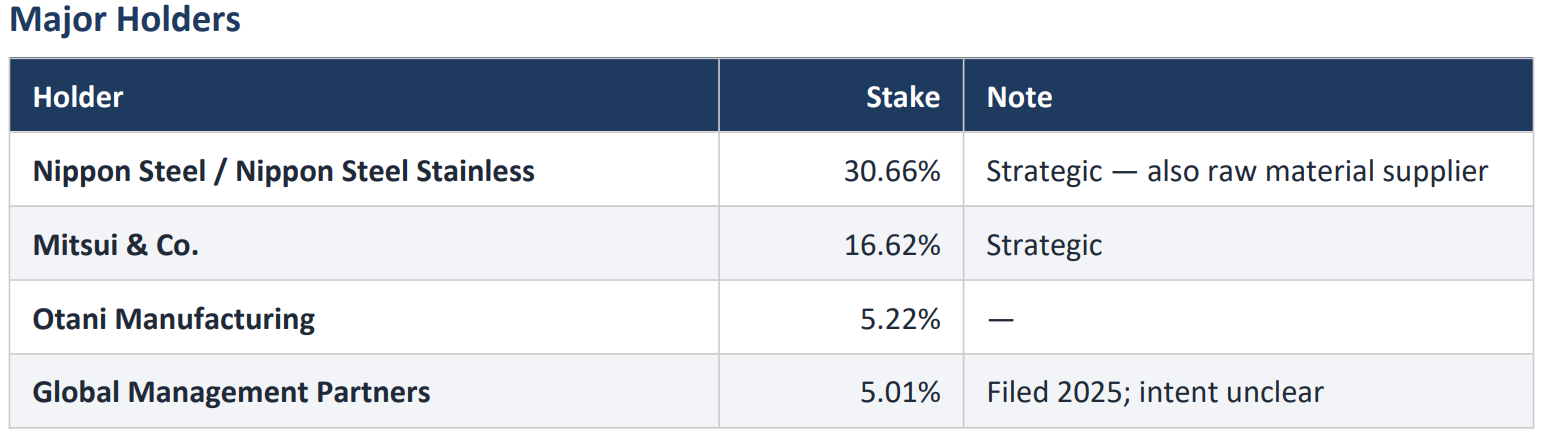

No room for activists as 30.72% owned by Nippon Steel and 16.65% by Mitsui. In October 2025 a Hong Kong firm named “GLOBAL MANAGEMENT PARTNERS LIMITED” appeared on the shareholder register with a 5% stake. No idea what their plan is, but this seems nearly activist proof.

The company reported a massive ¥2.2 billion loss during the great financial crisis. This is significant vs the market cap. The company is much smaller today with 150 employees vs ~600 pre-GFC. I don’t think a massive loss like this is likely given their much smaller scale and consistent profitability over the last 12 years, but anything is possible.

This is not a cash-heavy NCAV. Inventories are roughly one-third of current assets, and much of the NCAV is tied up in working capital rather than cash. Inventories have remained around ¥2.5 billion for the last 5 years.

Wildly illiquid and small. This is MORE illiquid than some smaller stocks I’ve written up!

Conclusion:

This thing is just too cheap and holding it while nothing happens doesn’t hurt as we’re getting paid 4% a year. The company is sitting on valuable real estate in a prime logistics hub in Tokyo. It makes no sense to use it for low return steel processing. I own an above average basket sized bet here.

Disclosure: I own shares in Takasago Tekko (5458). The security could be sold at any point in time without prior notice. This is a small position as part of a broader basket of cheap Japanese companies so I haven’t dug too deep into this name. If I missed anything important, feel free to share in the comments. None of this is investment advice. Everything in this post is my own opinion and I could be wrong. Do your own due diligence.

Appendix (Deeper dive into our asset and why it’s likely worth much more than my conservative ¥8bn estimate):

Itabashi Factory Location

Our factory is located in an industrial/logistics pocket near National Route 17, the Metropolitan Expressway Route 5 corridor, and Saitama access. While it isn’t as prime as Tokyo Bay for logistics, there are institutional quality logistics assets nearby and the area is a popular in-demand logistics area. Our property is located at 1-1-1 Shingashi, Itabashi-ku, Tokyo. We have a comparable transaction from 2019 at 1-2-2 Shingashi, Itabashi, which is VERY close by (see image below):

Our BEST comparable which is very close by was a deal transacted in April 2019 where 67.5% of the purchase price was attributed to land. Land prices have increased significantly since, so this should be conservative. But even using the 2019 transaction as our benchmark values our property at ¥17.5 billion, more than double my conservative estimate in the writeup.

Some AI Analysis:

D Project Itabashi Shingashi is especially important because it is at 1-2-2 Shingashi, while Takasago is at 1-1-1 Shingashi. Its acquisition price was ¥12.3bn, appraisal value ¥12.4bn, land area 16,545 sqm, and the appraisal’s cost-method value split was 67.5% land / 32.5% building.

Daiwa House REIT’s more recent data show the property’s appraisal value at about ¥14.3bn–¥14.4bn in 2025–2026, above the original acquisition price, which supports the idea that this location has remained valuable rather than impaired.

MLIT commentary for the Shingashi industrial point says demand exceeds new supply, prices are rising, there is firm demand from users requiring a Tokyo location, and large logistics construction has been seen nearby.

Takasago’s own rental real estate appraisal provides an internal sanity check. The facilities table separately lists 9,506 sqm of rental real estate associated with the Itabashi site, while the rental real estate note discloses ¥3.8bn of fair value. The appraisal cannot be cleanly allocated parcel-by-parcel, but it is consistent with nearby public land prices and REIT appraisals suggesting that the separate 36,009 sqm factory site could be worth materially more than the ¥8bn assumed in the base case.

The current use of the Itabashi land is economically hard to justify. Takasago is earning low returns from a steel-processing business on land that nearby REIT transactions and institutional developments suggest is far more valuable as urban logistics real estate.

We also have a proof of concept of an old Nippon Steel site being converted into a modern logistics facility. LOGIFRONT Tokyo Itabashi, completed in 2024 by Mitsui Fudosan and Nippon Steel Kowa Real Estate on a former Nippon Steel factory site in Itabashi. This is literally next door and was an old steel facility! A Nippon Steel site too! Remember, Nippon Steel owns ~30.6% of Takasago Tekko! A company involved in redeveloping a former steel site happen to own 30.6 % of our company. (Technically Nippon Steel Kowa Real Estate was involved, but it’s part of the Nippon Steel complex)

Mitsui describes the project as located in a rare dedicated industrial zone inside Tokyo’s 23 wards, with a 91,000 sqm site, 250,000+ sqm floor area, and six above-ground floors. It is positioned as Tokyo’s largest logistics facility, with good access to the city; the site is 10 minutes from Nishidai Station, has 1.06 million people within 5km, and is about 2.7km from Nakadai IC.

Corporate Video:

I appreciate that you mention the current use is hard to justify. Valuable Real Estate is fine, but if it means closing the current business you need to think about that for business as a going concern. Not all businesses can survive a move though this one looks like it might

Great find—how on earth do you unearth something like this?? Kudos to you.

The key as usual with these situations is what the trigger event is (cf Sato Foods). 4% divvy is nice but the chance of Nippon Steel redevelopment seems low unless they announce consolidating production elsewhere. Even then, hard to see a profitable company like this just being wound up. Have you come across any precedents?