Sohu.com Inc (Nasdaq: SOHU): A Net-Net with $1.3B in Cash and Valuable Real Estate ($400m+) Trading at $460m Market Cap with a $150m Buyback

The cash is off-shore and founder owns 1/3 of outstanding shares and has bought back stock at higher prices.

This writeup was inspired by David Orr’s tweet about the U.S. listed Chinese company DouYu (Nasdaq: DOYU) paying out a $9.76 special dividend. The stock closed at $12.59 the day before and was $6.59 earlier in the year. Among Chinese ADRs with significant cash balances, SOHU is my favorite. I have followed this company on and off for a decade, being bullish during COVID and bearish until recently.

Warning: For those unfamiliar with Chinese equities, cash on the balance sheet alone is meaningless. To pay dividends or conduct share buybacks, cash must be held outside China, as money cannot freely leave the country. DOYU is funding their large special dividend with cash held outside China from their initial IPO’s proceeds. SOHU’s cash hoard is the result of proceeds from the sale of their search business to Tencent, which was paid to SOHU in the Cayman islands. Transferring cash from mainland China outside the country is difficult and requires permission from regulators. On paper it’s possible, but even mega caps like Alibaba struggle to do it. I consider all cash in China to be trapped.

I am bearish most Chinese equities and bullish only on net nets with cash outside China where management is willing to return cash.

Quick Pitch:

Market Cap: $460m ($14.21/share)

Cash, short term investments, and long term time deposits; $1.3b (latest 10-Q)

Total Liabilities: $826m

Net Sohu Value after all liabilities: $474m

Net Sohu Cash Value ignoring Tax liabilities: 955m (100%+ upside on just cash value)

Tax liabilities on the balance sheet can reasonably be ignored, as the vast majority will likely never need to be paid. Koneko Research breaks this down well in their December 2021 writeup on Sohu.

There’s a lot of value inside SOHU besides its cash including real estate in Beijing likely worth $400m or more as well as a gaming business that absolutely gushes cash (likely worth at least $1b), but for now we’re going to ignore those completely. ~100% upside on the cash alone is good enough and I think the stock does well from here based entirely on their ongoing buyback.

Why now? The $150m Buyback.

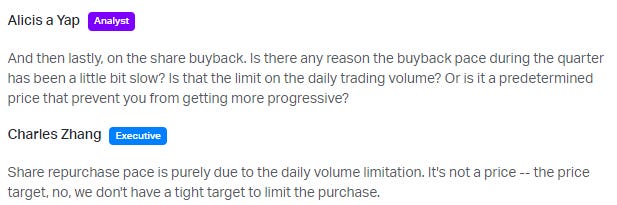

On March 2, 2024, SOHU increased the size of its buyback plan from $70m to $150m over the next two years. By February 29, they had repurchased $12M worth of shares, reaching $17m as of May 16. The sole limiting factor on the execution of the buyback has been daily volume as management has outlined in their latest earnings Q&A:

Daily volume being the limitation was emphasized in Q4 as well. Management specifically said they aren’t bound by price, but simply volume.

I’m inclined to believe management as SOHU’s stock price has marched steadily higher since the buyback was announced. The company seems to be a willing buyer and is repurchasing some percent of the daily volume, which is supporting the stock price. Keep in mind, the rise in SOHU stock is against a backdrop of flat Chinese stocks (BABA and JD are largely flat in the last 6 months).

The size of the buyback ($150m) is substantial given the small float, as a third of shares are owned by Charles Zhang, the founder and CEO, who has been buying back shares last year at much higher prices. Excluding the founder’s ownership, which likely isn’t for sale, $150m represents ~50% of the float.

At some point, I suspect Charles will try to take the company private or if he can’t do that, dividend out the cash as DOYU is doing. This wouldn’t be unusual as Charles has paid out huge dividends at companies he controlled before (namely Changyou which paid out over $1b before it was acquired by SOHU).

Risks:

Inside SOHU are 2 businesses. The Changyou business (gaming) is excellent and has been gushing cash for well over a decade and the Sohu business (media/video) which has been a massive money loser. The primary risk to SOHU is the company's potential allocation of increasing amounts of money to the struggling media business. Combined losses are currently meager relative to the company’s cash horde, but are expected to increase. Last year net loss was only $30m, but Q1 2024 was $25m and the company forecasts $30-$40m net loss for Q2. Annualized this is ~$140m. Just look at how terrible the media business is:

This is the major risk. The SOHU business has been terrible for a long time Charles, the founder and CEO, seems to love this side of the business. So much so that losses in this division almost bankrupted the company in the past. It was only when cash was running low that the he cut spending on the terrible media business and the company became profitable again. After selling their search business to Tencent SOHU found itself flush with cash again and began laying the foundations for taking another crack at the ultra competitive media/video business. It hasn’t been going well.

Still, despite the SOHU business being awful, Changyou continues to gush cash. On a standalone basis it’s likely worth at least $1b (5x 2023 operating profit). Likely much more, as peers trade at higher valuations in China. None of this matters though. SOHU stock is an interesting bet because the company is buying back stock on a daily basis which is supporting the stock price. The outcome of this investment is entirely on the company’s willingness to complete the $150m share repurchase program. I think management is sincere, but time will tell.

Conclusion:

I expect SOHU’s stock price to inch upwards as the company continues to buyback shares. I also expect Charles to eventually make a privatization bid for the entire company or if he doesn’t think it will succeed, large special dividends are a possibility. This is a small position, and I consider it riskier than many of the Japanese net-nets I’ve written about.

Disclosure: I own shares in SOHU. None of this is investment advice. Everything in this post is my own opinion and I could be wrong. Do your own due dilligence.

I use Koyfin for looking at historical data, screening, and visualizing financials. Koyfin offers real value to me and I have been a paid user long before they offered me an affiliate link with a 20% discount. The free version is excellent as well!

Very interesting. Can you point me to your source for the cash outside China? I am having trouble finding it in the annual report. thanks

damn, thats an interesting cpmpany. Thanks for the write up.

Any chance you might share your position size % considering the risks to refer to ?