3 Quick Pitches for 3 Deep Value Japanese Stocks: TOC (8841), Sankyo Kasei (8138), and Takase (9087)

TOC has tons of real estate, securities, and net cash. Sankyo Kasei is a DOUBLE net-net that repurchased 33% of outstanding shares this year, and Takase is a dirt cheap logistics co.

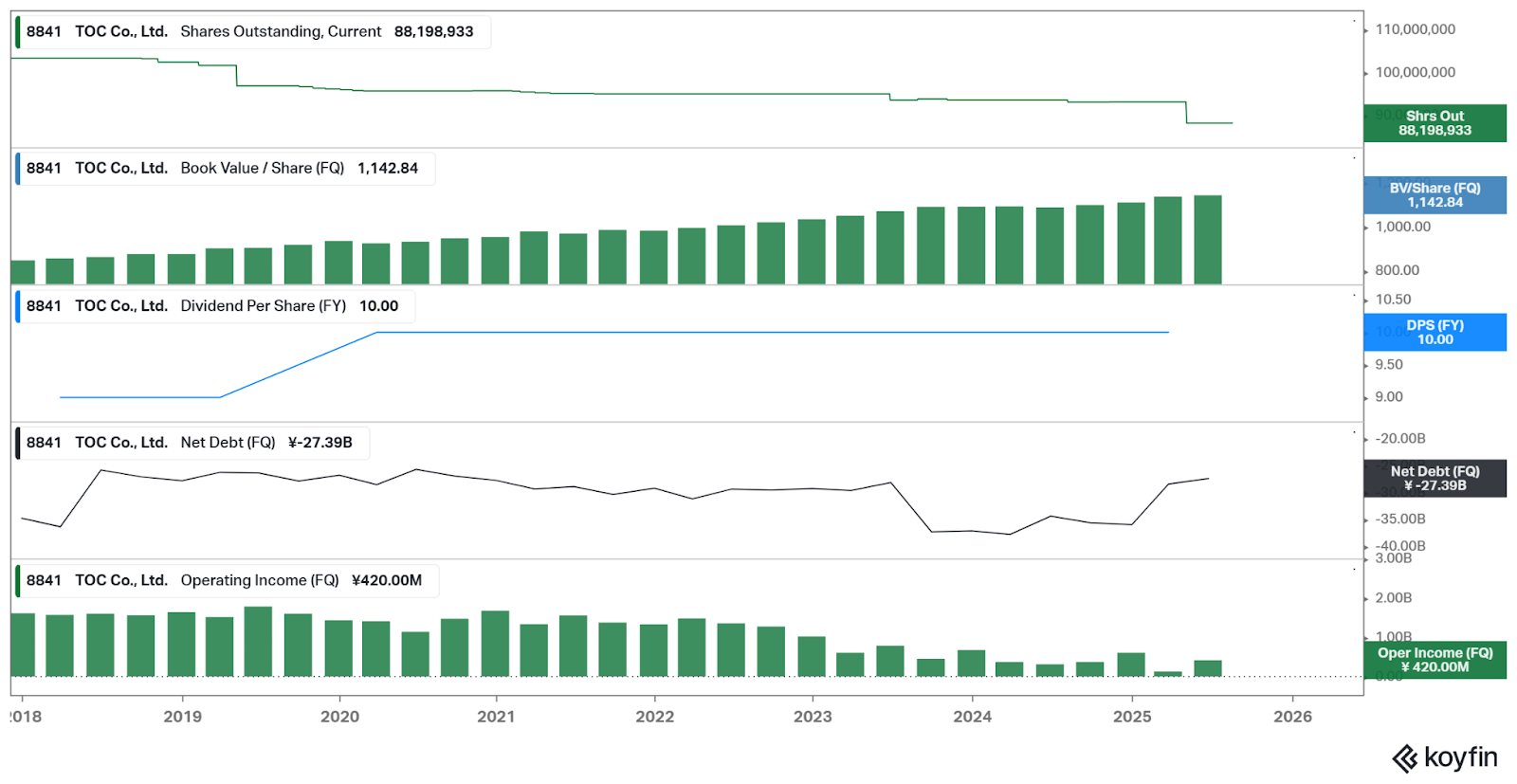

TOC Co. (TYO 8841)

Stock price: ¥801

Book value per share: ¥1,142

Market cap: ¥70 billion

NCAV+Inv Securities: ~¥42 billion

Adjusted Mcap: ~¥28 billion

Dividend Yield: 1.25% (¥10/share)

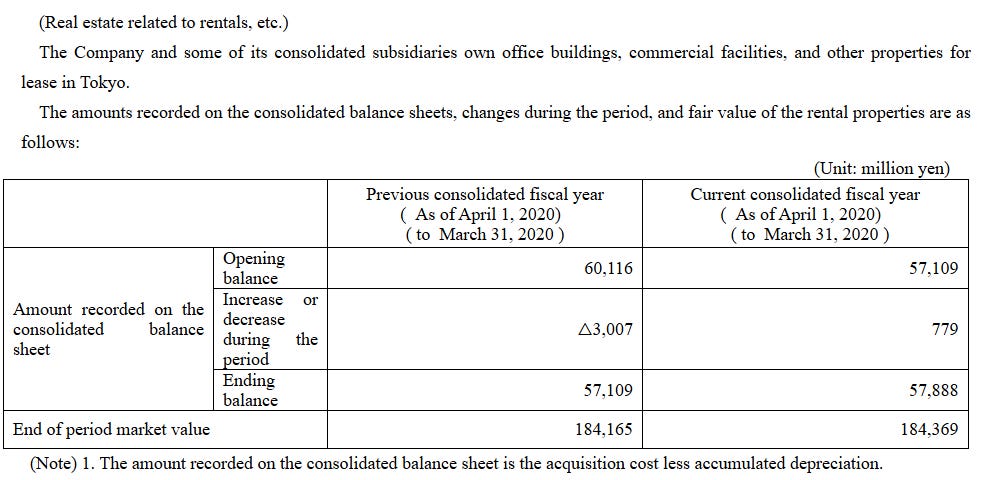

The pitch here is pretty straightforward. This is a real estate company in Tokyo that owns real estate assets worth significantly more than their carrying value. The company also has a large net cash position and investment securities, which are easy to value. Backing out the value of these assets gets us an adjusted EV of ~¥28 billion. ¥28 billion for ¥57.8 billion of real estate at book value isn’t a bad deal, but what makes this interesting is that the fair market value of the real estate (according to the company’s annual report) is ¥184.3 billion.

Figures from FY25 securities report:

Book value of real estate: ¥57.8 billion

Appraised fair value: ¥184.3 billion

Surplus above BV: ¥126.4 billion

Actual earnings aren’t that important as the real value lies in the assets. But the company is consistently profitable. Since 1985 they’ve only reported a net loss once, in FY2001. Earnings have dipped in recent years due to some poor planning surrounding their flagship TOC Building, which kicked out all of its tenants for a major redevelopment. The original plan was to demolish the aging building and better use the huge tract of land, but instead they did small renovations and reopened it. Re-leasing the property will take some time, but earnings are already improving and expected to increase significantly in the coming years. Capex related to earthquake-proofing a building also hit near-term profits.

There are other reasons to be bullish as well. Here are a few:

The company has done several buybacks over the years including a 5.31% buyback earlier this year.

Management tried to take the company private in 2007 for ¥800 per share (the same price as today!). A counter-bid came in at ¥1,100 which was later raised to ¥1,300. The competing bidder couldn’t get enough shares to tender to take the company private and it traded above management’s bid, so it remained public. Book value per share in 2007 was ~¥467 vs ¥1,124 today.

The founding family owns more than 50% of shares outstanding. The chairman, a member of the founding family, died in January. His estate will owe inheritance tax payable sometime in November. This could serve as a catalyst to ‘do something’. Taking the company private can be very advantageous for minimizing tax issues.

The company owns an 8.4% stake in New Otani, an unlisted hotel company, which is worth significantly more than its carrying value. All unlisted stakes for TOC are carried at ~¥0.85 billion, but just multiplying 8.4% by New Otani’s net assets is ¥7.6 billion. The company is likely worth much more given undervalued land. New Otani also earned ~¥10 billion in net income in FY24 and FY25.

I stumbled on this idea from Travis Lundy on SmartKarma. If you’d like to learn more about it, I strongly recommend reading his articles on it. They’re much more thorough. This is currently the biggest position in my cheap Japanese basket. While upside isn’t as large as some of the smaller names I own, the stock isn’t very volatile. It’s also more liquid than most of the names I write about.

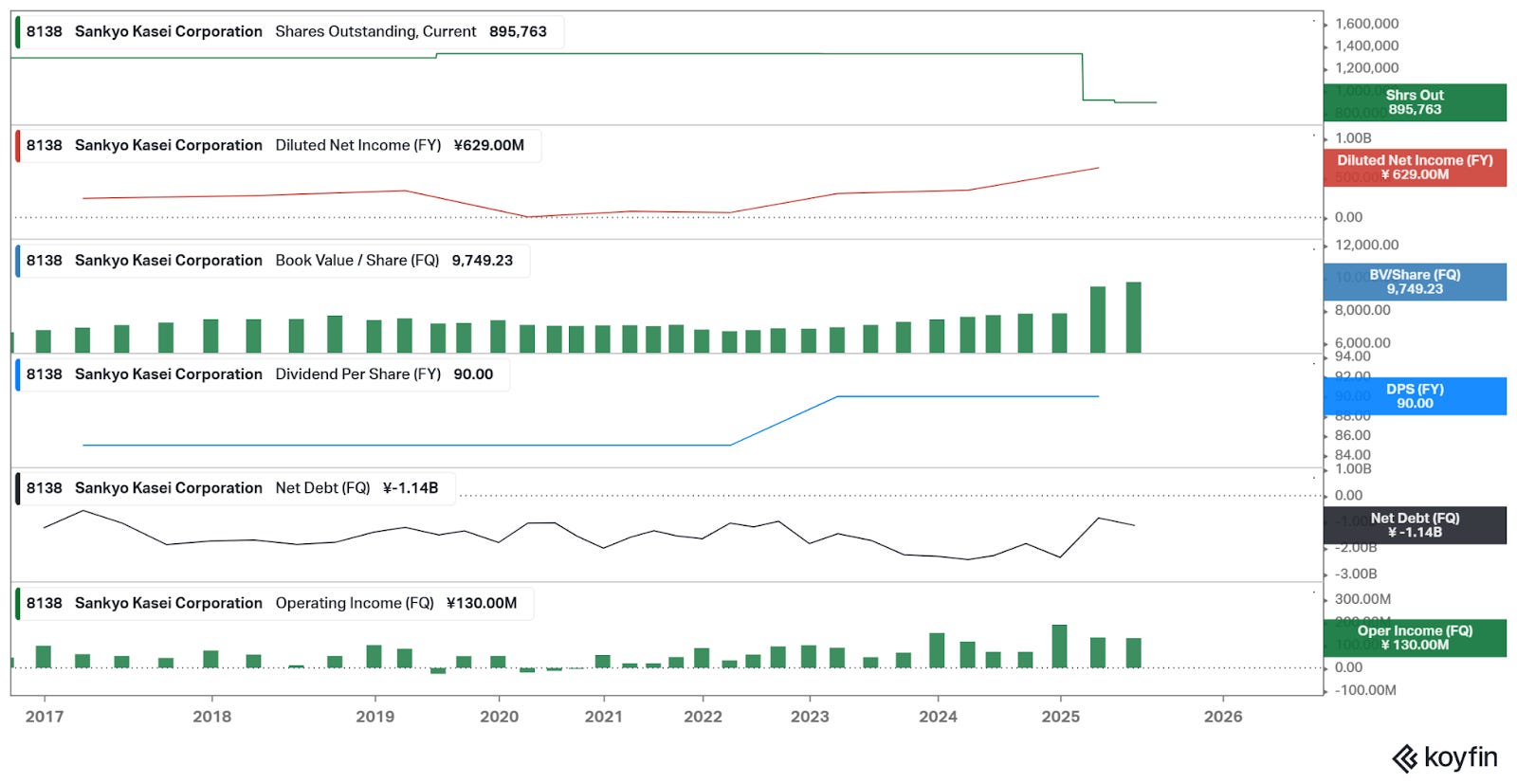

Sankyo Kasei Corp (TYO 8138)

Stock price: ¥3,890

Book value per share: ¥9,750

Market cap: ¥3.5 billion

NCAV+Inv Securities: ~¥7.1 billion

Adjusted Mcap: -¥3.6 billion

FY26 Net Income (Management forecast): ¥624 million (¥678/share)

FY26 Operating Profit (Forecast): ¥465 million

Dividend Yield: 2.5% (¥100/share)

Sankyo Kasei is a small trading company (middleman) that supplies chemicals and other materials to its customers along with technical expertise. The core business, while boring, has been consistently profitable. The value is in the balance sheet and the massive buyback earlier this year.

Here are the highlights

Double net-net valuation. Meaning the stock could double in price and still be valued at less than zero after backing out NCAV + investment securities.

Consistently profitable. Operating income has been positive since 1998 and has been mostly steady the entire time.

Massive accretive buyback. In February 2025, Sankyo Kasei repurchased 31% of outstanding shares, almost entirely from Black Clover and Swiss-Asia. These shares have since been canceled. In May 2025, the company repurchased another 2.5% of outstanding shares. Shares outstanding have fallen from 1,333,699 to 895,765.

There’s some parallel here to Mansei which also did a giant buyback (also from Black Clover). Black Clover’s strategy seems to be to buy up a sizable stake in cheap companies then offer to sell back to the company at near market price, profiting from the price uplift from their own buying. While an interesting strategy, they’re leaving a lot of money on the table and creating value for remaining shareholders.

While margins are pretty terrible (1.7% EBIT margin), they’ve been rising in recent years.

The company’s head office is in Osaka and sits on 492 sqm of land in a pretty good location. Book value for the land is ¥242 million. If we include the building, the head office + land is booked at ¥952 million. The land alone is easily worth double this figure.

This is a 1.5x-sized basket position. It is illiquid, so be careful!

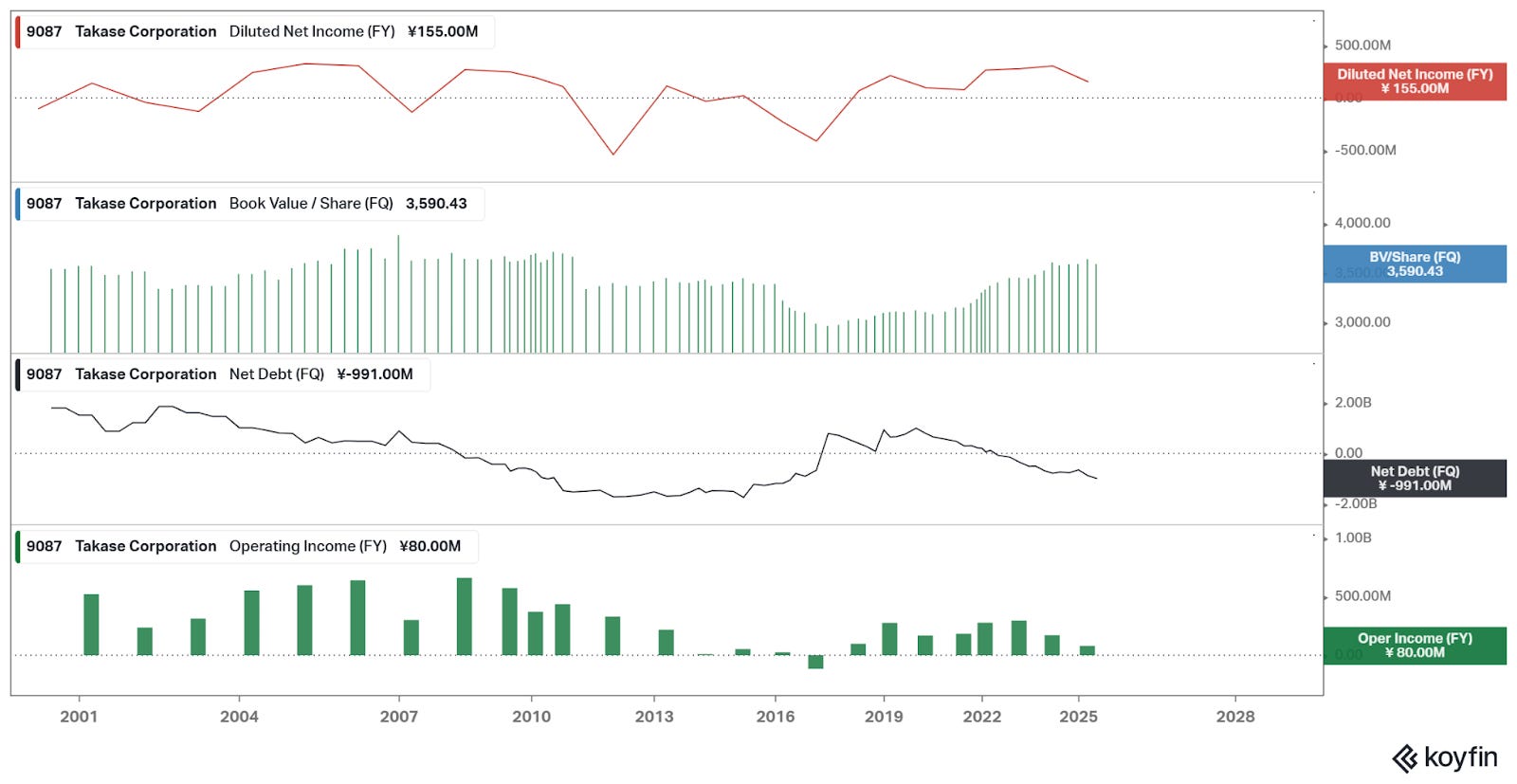

Takase Corporation (TYO 9087)

Stock price: ¥1,248

Book value per share: ¥3,590

Market cap: ¥2.5 billion

NCAV+Inv Securities: ~¥1.8 billion

Adjusted Mcap: ~¥700 million

FY26 Net Income (Management forecast): ¥180 million (¥89/share)

Dividend: 2.8% (¥35/share)

Takase is yet another small cheap logistics company. Readers and followers on X should know by now that I’m a fan of the sector, especially since the biggest win in the Japanese basket was Nissin Corp (9066) which I wrote about last year. It’s up 80% since then, but it’s a name I’m up over 200% on, as I bought it in early 2024.

While Takase isn’t as consistently profitable as other logistics names I like (such as Keihin 9312 and Nanso Transportation 9034), its small size and tiny adjusted market cap relative to the fair market value (FMV) of its assets give us a lot of upside.

Here are the highlights

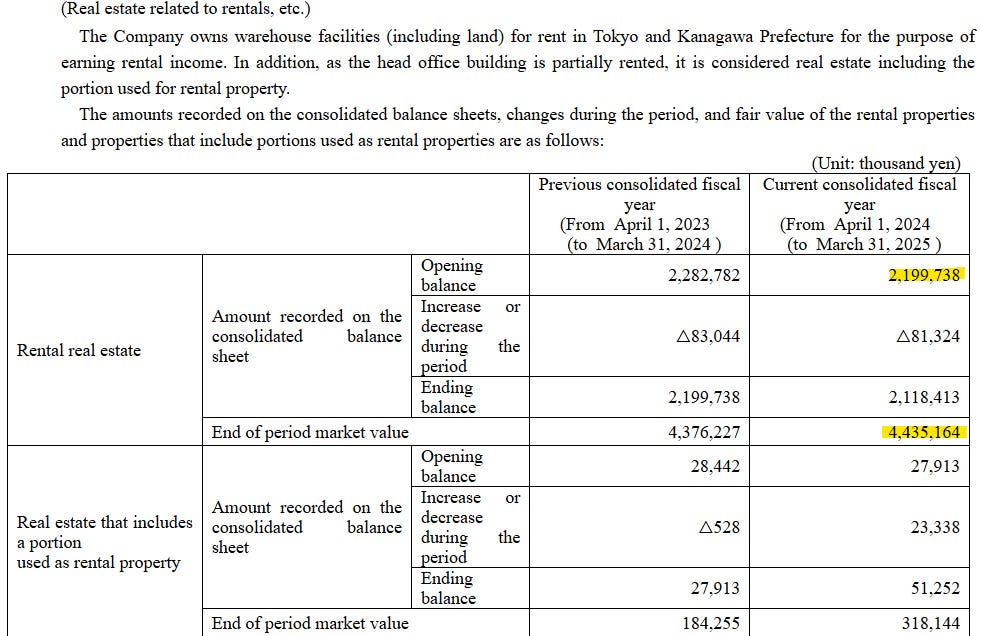

Takase owns logistics assets in Sapporo, Tokyo, and Kawasaki. Some properties are leased out to third parties to generate rental income while others are operated by the company. The rental assets have a book value of ¥2.1 billion but fair value is ¥4.4 billion, which is an uplift of ¥2.3 billion (vs a market cap of just ¥2.5 billion and adjusted mcap of ¥700 million!). There is no clear breakdown of which properties are rented out vs owner-operated except for rental properties being located in “Tokyo and Kanagawa.”

This FMV uplift is only for their rental assets. Owner operated properties do not have a fair value disclosure. Some properties have an overlap with a portion of the property leased out to third parties, and those also include a fair market disclosure that shows an additional ¥266 million uplift. The individual properties included in this FMV uplift are not disclosed.

The core operating business is not nearly as good as Keihin (9312), Nanso Transportation (9034) and other logistics companies I like. The company has been profitable on an operating income basis every single year since 1988, except for an operating income loss of 115 million in FY2017. However, operating income has been declining for decades, and net income has swung to losses many times.

Even if we assume zero further uplift from their entirely owner-operated assets, this is pretty cheap. Given the nanocap size and less consistent operating business, this is a much smaller position for me than many other Japanese logistics companies in my portfolio. My Keihin (9312) and Nanso Transportation (9034) positions, for example, are multiples larger than my Takase position. Takase is a half-basket sized position. While I haven’t written about Nanso Transportation on Substack before, I’ve posted about it on X.

While ‘undervalued land asset’ plays can be interesting, I don’t like making bets in the space unless the operating company is consistently profitable. One idea I passed on recently was Omikenshi (3111). For a quick look at that idea, click the link below to my X post.

I use Koyfin for looking at historical data, screening, and visualizing financials. Koyfin offers real value to me and I have been a paid user long before they offered me an affiliate link with a 20% discount. The free version is excellent as well! I don’t charge for access to my writeups. I wouldn’t promote something unless I really loved it and I love Koyfin.

Disclosure:I own shares in 8841, 9087, and 8138. These securities could be sold at any point in time without prior notice. These are small positions as part of a broader basket of cheap Japanese companies so I haven’t dug too deep into any of these names. If I missed anything important, feel free to share in the comments. None of this is investment advice. Everything in this post is my own opinion and I could be wrong. Do your own due diligence.

TOC is just insane. How can it be possible for a company to trade at an EV of ~¥500 with ¥2100 in real estate, ¥150 in listed investments and an unlisted stake likely worth >¥100, with previous takeout offers 30% above the current price, buying back stock and have an obvious catalyst in change of ownership?

Great work.